How Would Capping Credit Card Interest Rates Affect the ARM Industry?

On May 9, 2019, Senator Bernie Sanders (I-VT) and freshman Representative Alexandria Ocasio-Cortez (D-NY) introduced legislation that would levy restrictions on the interest rate credit card grantors could charge consumers. Specifically, the bill would establish a blanket limit on credit card interest rates at 15.0%, in addition to allowing post offices to offer financial services, such as checking or savings accounts, debit cards, low-interest loans, and check cashing. The proposed cap on credit card rates is of interest to the accounts receivable management (ARM) industry, as it could reduce the overall volume of credit card debt as well as the number of card originations – thereby lessening opportunities for collectors.

Credit Cards and ARM

What the Bill Would Change

Credit card interest rates are often much higher than 15.0% ceiling proposed by Sen. Sanders and Rep. Ocasio-Cortez. According to CreditCards.com, the average annual percentage rate (APR) on a new card (17.7%) is the highest the company has recorded since it first began tracking data in 2007. That is 1.0 percentage points higher than a year ago (16.7%) and 2.5 percentage points greater than in May 2016. Borrowers with a poor credit score face even stiffer rates; the APR for consumers with sub-prime credit scores is a whopping 25.3%.

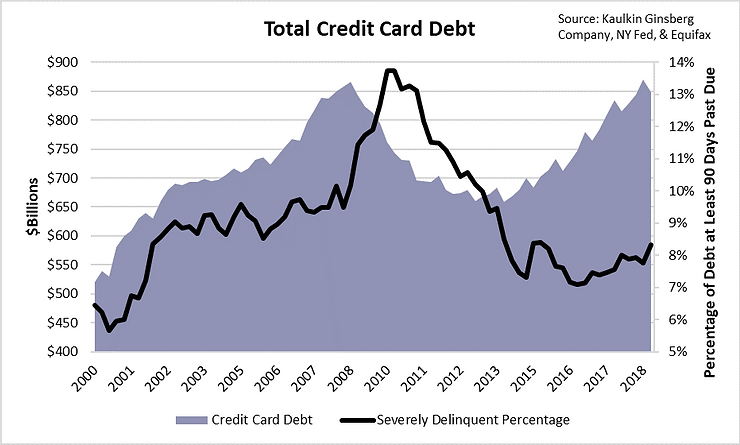

The 15.0% cap would affect the ARM industry in multiple pertinent ways. First, it would cause overall credit card debt balances to fall. Credit grantors charge interest to card holders who carry a balance from month-to-month. The higher the APR, the greater the amount of interest to be paid, leading to a growing total balance. If interest rates are limited to no more than 15.0%, borrowers may pay less interest than they would otherwise, thereby diminishing their potential debt burden. Not only would this improve these borrowers’ chances of avoiding severely derogatory delinquencies, but it would also decrease the dollar value per credit card account serviced by ARM companies, since there would be less debt to collect.

Second, the suggested rate ceiling may depress loan originations. Currently, banks and other credit card grantors use high interest rates to account for the risk of lending to borrowers who are less likely to repay compared to more financially stable borrowers. If interest rates were capped, credit grantors would have to either account for that risk in other ways, such as raising fees, or cease lending to high-risk applicants altogether. Since the former would anger the public and may invite regulatory intervention, credit grantors may simply choose the latter. As a result, the number of risky consumers with credit card accounts could dramatically decline.

Broader Implications

While the legislation has virtually zero chance of passing this Congressional session, on account of Republicans controlling both the White House and Senate, it does provide a peek at a potential direction the Democratic party could take if it were to control the three major Federal Government bodies. Sen. Sanders waged a prominent – albeit unsuccessful – presidential primary campaign against eventual Democratic nominee, Hillary Clinton, in 2016 and is running for president in 2020. Rep. Ocasio-Cortez, meanwhile, is a rising star among progressives, thanks to her ability to connect with Millennials, Generation Zs, and minority constituents. In a recent survey of potential Democratic primary voters, Emerson Polling found that 18-29 year-olds favored Sen. Sanders over the front-runner, Joe Biden, by 30 percentage points. In this sense, the Sen. Sanders’ and Rep. Ocasio-Cortez’s platforms may represent the future of the Democratic party and U.S.

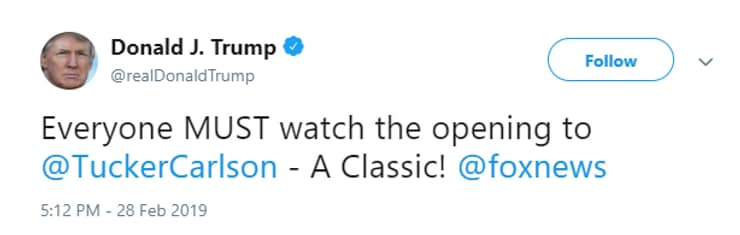

In addition, Sen. Sanders and Rep. Ocasio-Cortez may find unlikely allies in the populist wing of the Republican party. Notable Fox News host Tucker Carlson, for example, praised the duo as “absolutely, indisputably right” in their attempt to cap card rates. Though Mr. Carlson may not have any legislative power, he does have the ability to shape the national conversation. His show, Tucker Carlson Tonight, drew 3.03 million total viewers per showing in March 2019, second only to Sean Hannity in all of cable news. Additionally, Mr. Carlson seems to have the ear of President Trump, judging by his twitter account.

While the ARM industry and its credit-granting clients should not necessarily panic about interest-rate ceilings any time soon, they should start to contemplate regaining control of the public debate. Once a bill like this passes, it may be too late.