By, Michael Lamm, Managing Partner, Corporate Advisory Solutions, LLC

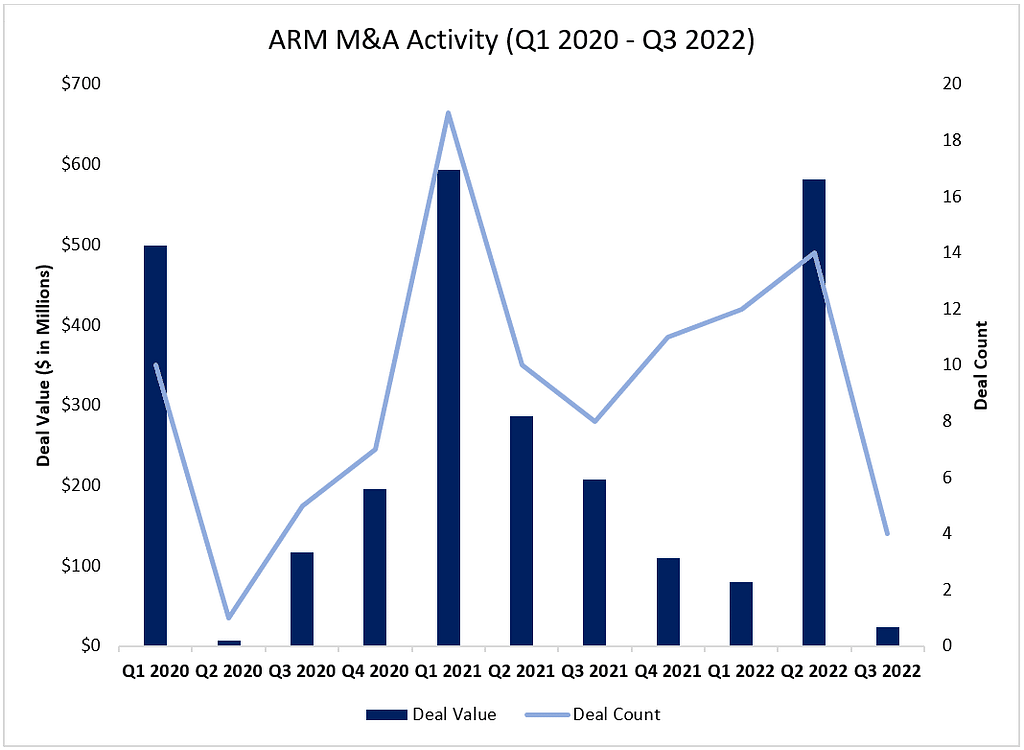

In Q3 2022, merger and acquisition deal volume in the Accounts Receivable Management (ARM) vertical experienced one of the slowest quarters since the start of the pandemic in Q1 2020. The industry saw a 50% decrease in Y-o-Y deal volume compared to Q3 2021 and a 71% decrease from Q2 2022. This contraction is due to the current market dynamics where placement volumes are increasing from previous years of artificially low charge-offs while liquidations continue to decrease across most asset classes. According to the Federal Reserve Bank of New York, credit card balances in Q3 2022 saw a $38B increase compared to last quarter and a $121B increase from Q3 2021, nearing pre-pandemic levels with a total of $93B. The 15% Y-o-Y increase represents the most significant increase in more than 20 years. Overall, total non-housing outstanding credit continued to grow in Q3 2022, reflecting the robust demand amid higher prices of goods and services. However, though delinquency rates are rising, they remain low by historical standards and suggest consumers are managing their finances through this period of increasing prices.

Student Loan Forgiveness Pending

A trend CAS has continued to monitor is the pending student loan forgiveness being ushered along by President Biden’s executive order. At the time of this newsletter, there have already been 26M applications filed on the federal application portal. The forgiveness plan is being appealed in federal court after various groups, including the states of Arkansas, Missouri, Nebraska, Iowa, Kansas, and South Carolina, have filed petitions regarding the constitutionality of the executive branch authorizing a plan of this scope and magnitude without Congress approval. The Biden Administration recently announced the pause in student debt repayment would be extended while the case is pending, potentially until June 30th, 2023.

Consideration of Buy Now, Pay Later

CAS continues to track the rise of buy-now, pay-later (BNPL) or point-of-sale credit extension. The CFPB recently issued its latest thoughts on the industry, expressing concerns that the Federal Reserve currently omits BNPL in its measurement of total outstanding debt. When considering the potential rise in delinquencies to come in the unsecured credit card vertical, the rapid growth of BNPL could be a potential giant lurking in the shadows of delinquencies that might exacerbate the issue. Although data is yet to be released for 2022, per the CFPB, charge-off rates in BNPL have increased from 2.9% in 2020 to 3.8% in 2021. Considering that charge-off and delinquency rates were falling in the credit card vertical during that time, a potential narrative begins to weave together. This trend has the potential to be an early warning for the broader economy if charge-offs continue to rise in the BNPL vertical.

Signs of Investor Interest Growing

Despite the decrease in deal volume for Q3 2022, there continues to be growth in investor interest in the ARM technology vertical. New entrants to the market are coming from international domiciles with interest in entering various stages of the delinquency cycle. Companies like Sedric are working to automate and optimize the compliance protocols and procedures of agents in collection agencies, ArborKnot is taking a “consumer friendly’ approach to debt purchase, and Retrieval Alliance is taking a technology focused approach to commercial receivables. These companies signify a trend that we at CAS feel is validated; that there is market interest in the U.S. ARM vertical given the sizeable market opportunity as we gear up for a potential economic downturn.

Conclusion

To conclude, after the ARM vertical experienced record years of M&A activity fueled by government stimulus, deal activity hit the brakes in Q3 of 2022 as companies will continue to evaluate their new normal throughout the remainder of the year. CAS expects 2023 to be a growth year for the ARM market compared to 2022. This means that now could be a good time for owners to start formulating an exit strategy. Strategic and Financial buyers will continue to remain interested in M&A opportunities and will be more motivated once growth trends return.