NY STATEWIDE DEBT COLLECTION LICENSING BILLS RETURN

New bills in New York, Assembly A5537 and Senate S4271, would create a statewide licensing requirement for third-party collection agencies, debt buyers, and other covered entities collecting consumer debt from New York residents. Covered companies would need to apply for and maintain a license, provide ownership and control details, pay licensing and renewal fees, and comply with ongoing reporting requirements under a state regulator’s oversight. If enacted, this would add a new layer to the existing patchwork of state licensing and federal requirements, increasing operational complexity for firms that collect nationally but have limited New York activity. Similar proposals have been introduced in prior sessions without advancing, but the reintroduction signals continued legislative interest in expanding New York’s oversight of debt collection.

WA MOVES TO RESTRICT MEDICAL DEBT COLLECTION AND CREDIT REPORTING

Washington lawmakers introduced two bills that would sharply limit medical debt collection leverage. SB 5993 would prohibit charging or collecting interest on new or unpaid medical debt and would tighten post-judgment enforcement timelines for judgments that include medical balances. HB 1632 would ban medical debt from consumer credit reports in Washington and would prohibit providers and collectors from furnishing medical debt to credit bureaus. Medical debt reported in violation of the proposal would be void and unenforceable, and new medical debt contracts would need specific language stating the debt cannot be credit reported or the contract could be void.

UPCOMING WEBINAR: TAX & RISK ROUNDTABLE

As state and federal expectations evolve, tax planning and operational risk are becoming more closely linked, especially for financial services organizations navigating growth, audits, and changing business models. Cornerstone is partnering with Forward Firm for a roundtable focused on practical insights around tax exposure, common internal disconnects, and how to reduce surprises.

We will cover recurring pressure points for lenders, servicers, mortgage companies, debt collectors, and fintechs, with real-world examples of how misalignment across finance, legal, and operations can create challenges during audits, exams, and transactions.

We will cover recurring pressure points for lenders, servicers, mortgage companies, debt collectors, and fintechs, with real-world examples of how misalignment across finance, legal, and operations can create challenges during audits, exams, and transactions.

We’ll discuss:

- State and local tax exposure tied to business activity and footprint

- Common cross-team gaps that create avoidable risk

- Planning ahead of expansion, M&A, or new launches

- Recent state audit trends Forward Firm is seeing in financial services.

REGISTER NOW

STATES EXPAND EWA OVERSIGHT AND LIMIT COLLECTION TOOLS

Oklahoma, New Jersey, Arizona and Colorado have introduced earned wage access bills that move the product toward a regulated, licensed model with standardized consumer protections. Across the proposals, providers would generally need clear fee disclosures, a no-cost access option, complaint handling, privacy safeguards, and fee-free cancellation. The bills also share major restrictions, including limits on using credit reports for eligibility, charging late fees or interest-like penalties, reporting nonpayment to credit bureaus or debt collectors, and pursuing repayment through lawsuits or third-party collections, with narrow exceptions such as fraud. Timing and structure vary by state, but the combined trend is tighter supervision and reduced downstream collections pathways for EWA balances.

FL MEDICAL DEBT COLLECTION AND CREDIT REPORTING RESTRICTIONS

Florida SB 1222 would tighten limits on medical debt collection activity and restrict both lawsuits and medical debt sales unless the buyer and collector execute a detailed written agreement before any sale. The bill would prohibit a broad list of collection actions, including arrest threats, liens and foreclosure on real property, wage garnishment, tax refund offsets, bank account seizure, and furnishing medical debt information to consumer reporting agencies. It would also require the sale agreement to cap interest at no more than 2 percent per year and include procedures to return or recall debt if the consumer is later found eligible for financial assistance. If enacted, medical debt buyers, collectors, and healthcare creditors operating in Florida would need updated portfolio purchase terms, operational controls, and credit reporting procedures. The measure would take effect July 1, 2026.

2026 LICENSING CHECKLIST FOR FINANCIAL SERVICE BUSINESSES

NEW! A fillable, year-round planning guide to help regulated financial services businesses organize licensing obligations, owners, and deadlines.

What’s Included:

- Annual obligations overview

- Q1 baseline review

- Mid-year checkpoint

- Federal & periodic reporting

- Q3-Q4 renewal readiness

- Event-driven triggers

MN BROAD DEBT COLLECTION LICENSING REQUIREMENTS AFFIRMED

The Minnesota Court of Appeals upheld a cease-and-desist order against an out-of-state company for allegedly collecting in Minnesota without a collection agency license. The court said Minnesota’s licensing rules apply broadly to any entity seeking to collect payment on behalf of others, even when the company is located outside the state and the claim is framed as an assignment. In this case, attempting to recover rental-vehicle damage claims for Minnesota businesses, sending collection letters, holding funds in a trust account, and remitting proceeds to clients were treated as collection activity that requires licensure. The court also rejected arguments that the company was not operating in Minnesota or that the statute was unconstitutionally vague, emphasizing that collection tied to Minnesota businesses or transactions can trigger licensing even if the consumer resides elsewhere.

UPDATE: INTEGRITY FIRST INSURANCE

As we look ahead to 2026, several updates for our Cornerstone / Integrity First Insurance clients that are designed to provide better support, improved coordination across our services, enhanced coverage options, and create meaningful cost savings.

NEW PARTNERS

Additionally, after considerable vetting, we’ve added two new partners in response to feedback we’ve heard from many of you about challenges you’ve experienced with your existing vendors in these areas. We’ve scoured the country to find outstanding agencies capable of supporting all your insurance needs, and we’re excited to introduce these resources as additional options for you in 2026.

- High Net Worth Individual Insurance (Home, Auto, Umbrella, etc.)

- We now have an agency partner equipped to support high net worth personal policies with the level of service these accounts require.

- Corporate Healthcare Programs

- We have added a partner to support corporate healthcare program needs, with an emphasis on improving plan options and identifying savings opportunities.

MORE CONNECTED THROUGH ATLAS

We are expanding our platform so that insurance, bonds, and licensing will all be fully integrated into Atlas, our online portal. This will give you a clearer, centralized view of your full services and policies, and it will simplify how information is managed and shared between our team and yours.

ADDITIONAL SUPPORT

To support these initiatives, we’ve hired two key team members you may be working with more closely.

- Holly Irvin – Holly is a 20-year insurance pro w/ deep underwriting and technical experience across commercial P&C lines, especially cyber. She will be focused on strengthening market access, underwriting coordination, and program development.

- Andrea Woodbury – Andrea previously supported our Cornerstone surety bonds clients, and is now leading operational and process oversight for these programs to ensure execution, transparency, and consistent follow-through.

DEBT COLLECTION INDUSTRY REPORT

Tratta just released its 2026 Debt Collection Industry Report, The Reality Check: The Widening Gap Between Digital Ambition and Maturity, a snapshot of where the industry stands on modernization. The key theme: teams are eager to go digital, but many still lack the operational maturity to execute at scale, especially across agent tools, compliance/QA, conversion economics, and data integration.

Powered by Tratta’s Modern Collections Technology Index (MCTI) and aggregated insights from industry professionals, the report helps you benchmark your organization, pinpoint what’s holding performance back, and see how leading teams are sequencing modernization to improve results. Download the report to see how you compare to your peers and where the biggest opportunities are.

LICENSING ENFORCEMENT AND BORROWER-LOCATION THEORY GAINS MOMENTUM

California entered into a consent order with a crypto-backed lending platform over alleged unlicensed lending to California residents, reinforcing the state’s view that lending to residents triggers licensing obligations regardless of online delivery or collateral type. At the same time, a coalition of states supported rehearing in a Tenth Circuit case challenging Colorado’s borrower-location approach to where a loan is “made,” with broader implications for interstate lending models and bank-fintech partnerships. If borrower-location tests continue to spread, multi-state lenders may face a more fragmented licensing posture and higher operational burden. This is a key area to watch for licensing strategy, program structuring, and state-by-state risk assessments.

NY CRA OBLIGATIONS EXTENDED TO NONBANK MORTGAGE LENDERS

New York DFS adopted regulations extending Community Reinvestment Act style obligations to certain nonbank mortgage lenders licensed in the state. Effective July 7, 2026, DFS-licensed mortgage bankers that originated 200 or more New York mortgages in the prior year will need to demonstrate fair and equitable access to home loans, with emphasis on low and moderate income communities. This adds a new layer of state expectations for nonbank mortgage originators operating at scale in New York. Firms should begin assessing whether they will meet the volume trigger and what reporting and examination expectations may look like.

AZ STUDENT LOAN SERVICER LICENSING AND OMBUDSMAN PROPOSAL

Arizona lawmakers introduced HB 2302, which would create a Student Loan Ombudsman within the Department of Insurance and Financial Institutions to receive and help resolve borrower complaints, analyze complaint trends, and monitor student lending laws. The bill would also require most student loan servicers to obtain a state license, with exemptions for banks, credit unions, and their wholly owned subsidiaries, and would set a biennial renewal cycle with record-retention requirements. It adds specific conduct standards for servicers, including prohibitions on deceptive practices, misapplying payments, furnishing inaccurate credit reporting information, and refusing to communicate with a borrower’s personal representative. The proposal also imposes operational requirements around payment application instructions and servicing transfer timing, and authorizes civil penalties up to $100,000 per violation. The measure would take effect only if approved by a two-thirds vote in both chambers, and if so, would become effective immediately.

CA DFPI COMMERCIAL FINANCING REPORTING DEADLINE

California DFPI set a March 15, 2026 deadline for certain commercial financing providers to submit an annual Commercial Financing Annual Report. The requirement applies to entities offering commercial financing or related financial products or services to small businesses or nonprofits, where the activity is principally directed or managed from California. Covered providers should confirm whether they fall within scope and ensure reporting processes and data collection are in place ahead of the deadline.

OR STATE AND CITY ENFORCEMENT TARGETS SMALL-DOLLAR PRICING AND BANK PARTNERSHIPS

Oregon resolved allegations against nonbank participants in a bank-partnership secured-vehicle lending program, asserting that state rate caps, licensing requirements, and contract restrictions applied despite bank origination and funding. The consent order required more than $1.5 million in borrower restitution and reflects a willingness to challenge program economics and contract terms through state-law theories that do not hinge on who funded the loan. Separately, the City of Baltimore filed a civil action against a fintech offering a small-dollar cash advance product marketed as earned wage access or overdraft-style liquidity, alleging fees effectively turned the product into high-cost lending and obscured the true cost. These actions highlight a growing compliance risk map where local authorities can become early movers and push theories that treat fees as interest equivalents.

MD VIRTUAL CURRENCY KIOSK RULES FINALIZED

Maryland finalized regulations implementing its virtual currency kiosk statute, establishing detailed requirements for registration and ongoing operation of kiosk operators and individual kiosks statewide. The framework builds on statutory obligations that begin January 1, 2026, and is a clear compliance trigger for any business offering or placing crypto kiosks in Maryland. Fintechs and kiosk operators should review registration scope, operational controls, and any consumer-facing disclosure or transaction requirements in the rules to avoid enforcement risk.

VIRTUAL SUGGESTION BOX

We’ve continued to hear great feedback from you, our clients, on how our newsletter provides value for your organization. To ensure we continue to research and provide the best data, we have created a virtual “suggestion box” for your ideas. Whatever topic you’d like to learn about, large and small, we will go research with our team and knowledgeable folks from our industry.

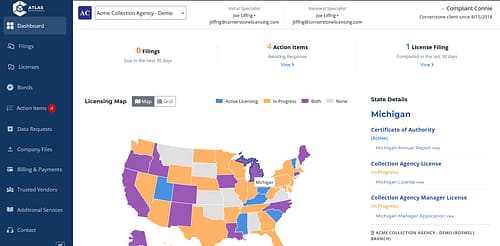

NEW ATLAS DASHBOARD: NOW LIVE

For clients using the Atlas licensing management portal, a new dashboard is now live when you log in. It provides a visual view of your licensing status by state and highlights key items at a glance, including upcoming due dates, upcoming action items, and recently completed filings. As part of our ongoing effort to make Atlas more useful and intuitive, we are making consistent improvements that help you find what you need faster and stay ahead of what is coming next.

LOGIN TO ATLASIN CONSUMER LENDING CODE OVERHAUL

Indiana SB 169 would reorganize and recodify multiple consumer lending statutes into a new consumer lending code, including provisions that currently govern first lien mortgage lending, small loans, and home loan practices. For mortgages, it authorizes the Department of Financial Institutions to adopt licensing rules for creditors and mortgage loan originators aligned with the federal SAFE Act and would require annual license renewal by December 31, with defined grounds for denial, suspension, or revocation. The bill also updates foreclosure consultant rescission rules and restricts replacing certain subsidized or low-rate loans with high-cost home loans within the first 10 years without written consent from the holder. For small loans, it would require licensing to make, take assignments on, or directly collect small loans, impose term and repeat-borrowing limits, set finance charge caps with inflation adjustments, and limit what lenders can recover after default. The proposal would take effect July 1, 2026, with one section set to expire June 30, 2028.

BEYOND THE NEWSLETTER

Head to LinkedIn and give us a follow to tap into a stream of real-time updates, legislative changes, and great content tailored for ARM and Fintech professionals. Engage with thought leaders and peers in our community to enhance your expertise.

Follow Cornerstone on LinkedIn and transform the way you stay informed in our ever-evolving industry.

EDUCATION DEPARTMENT PAUSES INVOLUNTARY COLLECTION TO IMPLEMENT REPAYMENT REFORMS

The U.S. Department of Education announced a temporary delay on involuntary collection tools for defaulted federal student loans, including administrative wage garnishment and Treasury offset, while it implements repayment reforms. Defaults will still be reported to credit bureaus, and borrowers are encouraged to consolidate, select repayment options, or pursue rehabilitation during the pause. New repayment changes are scheduled to begin July 1, 2026, including a streamlined repayment structure and interest-waiver features for certain on-time payments. For debt collection stakeholders, this may change near-term federal student loan recovery volume and servicing timelines.

NJ LICENSING PATH FOR FOR PROFIT DEBT ADJUSTERS

New Jersey AB 4598 would allow certain for profit debt adjustment companies to become licensed to operate in the state, but only if they do not receive or hold consumer funds and are regulated by the FTC under the Telemarketing Sales Rule. The bill defines a debt adjuster as an intermediary that negotiates or alters debt payment terms between a debtor and creditors and applies the same operating rules and restrictions that currently apply to nonprofit entities, with some differences in audit and bonding requirements. It authorizes the Commissioner of Banking and Insurance to set maximum fees and requires annual reporting on enrolled consumers, fees collected, and total debt settled. The measure also adds detailed contract disclosure requirements about services, fee calculations, timing expectations, and limits on providing legal, tax, or accounting advice.

CA DFPI ENFORCES LENDING LICENSING FOR CRYPTO BACKED LOANS

California DFPI announced a penalty against Nexo Capital Inc. for allegedly making thousands of crypto-backed consumer and commercial loans to California residents without a California Financing Law license and without evaluating ability to repay. The action reinforces DFPI’s view that offering lending products to California residents triggers licensing and underwriting-related obligations even when products are collateralized by digital assets. The order also required moving California resident funds to an affiliated entity that holds the relevant state license. This is a key signal for fintechs offering novel credit structures that state licensing and consumer finance requirements still apply.

CA MORTGAGE ENFORCEMENT FOR UNLICENSED MLO ACTIVITY

On December 31, 2025, the California DFPI entered a consent order with a residential mortgage lender over alleged unlicensed mortgage loan originator activity under California law. The lender agreed to a $160,000 administrative penalty and to additional review and remediation steps without admitting wrongdoing. The action reinforces that license scope, individual credentialing, and internal monitoring for origination activity remain high-risk areas.

MD MONEY TRANSMITTER DEFINITION CHANGE FOR PAYROLL AGENTS

Maryland HB 118 would amend the Maryland Money Transmission Act to exclude certain payroll processing arrangements from the definition of a licensed money transmitter. The exclusion would apply when a person is designated as an employer’s agent for payroll services under a written agreement, the employer presents the agent as providing payroll processing, and the employer remains responsible if the agent fails to deliver funds to employees or other payees. This proposal could reduce money transmitter licensing exposure for some payroll processors and payroll service vendors operating under an agent of payor model in Maryland. If enacted, the change would take effect October 1, 2026.

CFPB NMLS SYSTEM CHANGES AFFECT MORTGAGE REGISTRY DATA

The CFPB proposed updates to its Privacy Act notice for the Nationwide Mortgage Licensing System and Registry, clarifying expanded use of the system for registration and administration activities tied to covered institutions. The proposal would broaden the categories of individuals covered, including certain primary contacts and administrative users, and expand the types of records collected to include more identifying information. Mortgage lenders and federally regulated institutions that use NMLS administrative functions should track the scope of data elements and retention terms described in the notice. Comments are due February 17, 2026.

NY LLC TRANSPARENCY ACT FOR FOREIGN LLCS

Effective January 1, 2026, New York requires LLCs formed outside the United States that are authorized to do business in New York to file either a beneficial ownership disclosure statement or an attestation of exemption with the Department of State. Foreign LLCs newly authorized on or after January 1, 2026 must file within 30 days of their application for authority, while previously authorized foreign LLCs must file by December 31, 2026. Filings are electronic, required annually, and subject to a fee, with penalties that can include monetary fines and possible suspension for noncompliance.

AI AND STAGED MEDIA FRAUD RISKS FOR LENDERS

Lenders are seeing a rise in borrower-submitted photos and videos that look legitimate but may be staged, altered, or generated using AI. This creates a growing fraud risk because traditional review methods can struggle to spot manipulated media. Industry groups are responding with training resources focused on recognizing and mitigating media-based fraud in underwriting and verification workflows. If your team is evaluating controls in this area, it may be worth reviewing available education and tools designed to help identify manipulated media before it drives losses.

TREASURY TARGETS MINNESOTA BENEFITS FRAUD WITH FINCEN AND IRS ACTIONS

The U.S. Department of the Treasury announced a set of actions focused on alleged government benefits fraud in Minnesota, including new investigative and reporting measures tied to money movement and suspected laundering. FinCEN issued notices of investigation to several Minnesota money services businesses and launched a Geographic Targeting Order requiring banks and money transmitters in Hennepin and Ramsey Counties to provide enhanced reporting on certain cross-border transfers of $3,000 or more. Treasury also said FinCEN issued an alert to financial institutions with red flags tied to fraud involving federal child nutrition programs and provided training to law enforcement on using financial data such as suspicious activity reports. The IRS is auditing financial institutions that allegedly facilitated laundering and plans to form a task force focused on pandemic-era tax incentives abuse and misuse of 501(c)(3) status connected to the schemes.

IL LICENSEES WARNED OF PHISHING SCAM EMAILS

The Illinois Department of Financial and Professional Regulation alerted licensees to a phishing scam email that asks recipients to confirm receipt of documents before sharing additional details. The Department flagged telltale signs including a deceptive reply to domain that is not an official Illinois.gov address, impersonation of a Department staff member, and phone numbers that do not match the agency. IDFPR emphasized it only sends emails from official Illinois.gov addresses and will not request confirmation of document receipt in this manner. Licensees should not reply, click links, or provide information, and should report suspected messages to [email protected]

OR DEBT RESOLUTION SERVICES REGISTRATION AND FEE RESTRICTIONS

If passed, Oregon HB 4141 would require debt resolution service providers to register with the Department of Commerce and Business Services and submit consumer agreement forms and proposed fee schedules. The bill would set detailed agreement content and disclosure requirements and require providers to provide or make available a copy of the agreement to consumers. It would also restrict fees so providers could not collect until a written agreement is in place, at least one debt has been negotiated or resolved, and the consumer makes at least one payment under the resolution. If enacted, providers would face annual reporting obligations, potential consumer liability for certain losses, and a surety bond requirement, with several specified exemptions. Most provisions would take effect January 1, 2027, with certain sections effective 91 days after legislative adjournment.

WY & FL STATE DIGITAL ASSET MOVES

Effective January 1, 2026, New York requires LLCs formed outside the United States that are authorized to do business in New York to file either a beneficial ownership disclosure statement or an attestation of exemption with the Department of State. Foreign LLCs newly authorized on or after January 1, 2026 must file within 30 days of their application for authority, while previously authorized foreign LLCs must file by December 31, 2026. Filings are electronic, required annually, and subject to a fee, with penalties that can include monetary fines and possible suspension for noncompliance.

This information is not intended to be, nor is it, legal advice. It is intended for information purposes only. We make no warranty, express or implied, as to the accuracy or reliability of this information. We are not attorneys. You must retain your own attorney to receive legal advice. While Cornerstone strives to provide the most current and accurate state licensing information, the responsibility for any decision related to state licensing or agency compliance is solely yours.